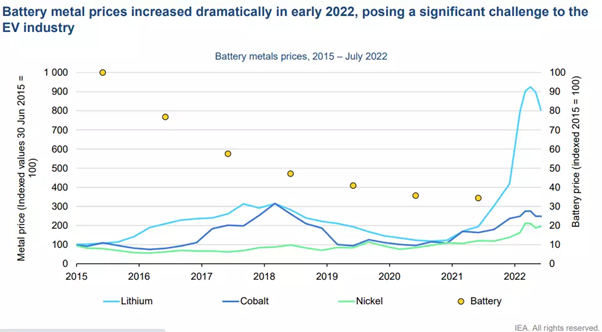

Lithium, nickel, and cobalt prices have skyrocketed this year due to the rising global demand for electric vehicles. The Paris-based autonomous intergovernmental body IEA has warned of a severe demand-supply imbalance in lithium in the coming years, underlining the need for large mining and refining operations. It also demonstrated the magnitude of China's lead and domination in this field.

Increasing strain on the supply chain of materials that go into EV batteries, coupled with an increase in global demand for EVs, has resulted in an unprecedented price increase for these materials this year. Lithium prices have increased by more than sevenfold in the first half of this year, while cobalt prices have more than doubled, and nickel prices have nearly doubled. Worse yet, this is likely to be a reoccurring issue in the future as the widespread adoption of electric vehicles puts strain on the supply chain, which cannot meet the demand.

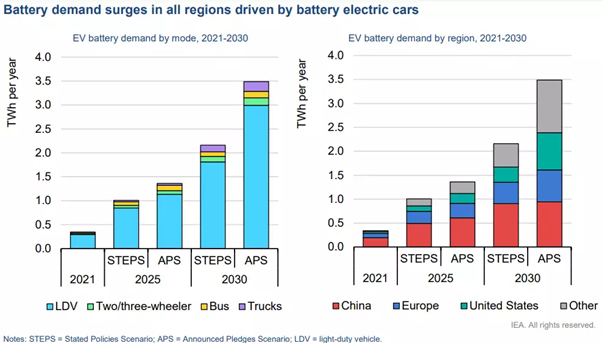

A recent report by the Paris-based autonomous inter governmental organization International Energy Agency (IEA) titled "Global Supply Chains on EV Batteries" highlighted the urgent need for massive investments in the mining and processing of key battery raw materials if the highly probable scenario of a severe demand-supply mismatch is to be avoided. From 340 GWh currently, the research predicts EV battery demand would increase to a conservative estimate of 2200 GWh by 2030 and an ambitious projection of 3500 TWh.

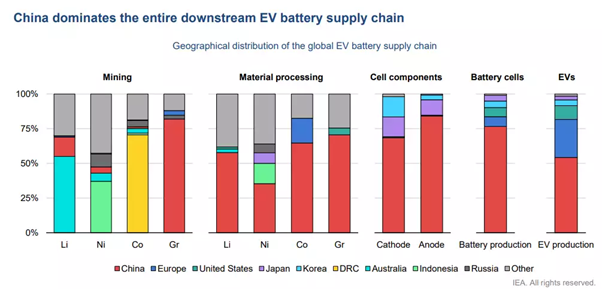

China processes more than half of the world's lithium, cobalt, and graphite raw materials. In addition, China controls the entire graphite anode supply chain, accounting for 80 per cent of worldwide graphite mining. China's 655 GWh of EV battery production capacity in 2021 represents 76% of the global battery production capacity. In addition, it has a head start in investing in future cell chemistries such as sodium-ion batteries.

The survey also underlined China's dominance throughout the whole battery materials supply chain. Currently, three-quarters of battery cell production capacity is located in China, and the same is true for the production of specialised cathode and anode materials, with China accounting for 70 per cent of cathode and 85 per cent of anode material global production capacity, respectively.

"By the end of the decade, EV batteries will account for between 70 and 80 per cent of worldwide lithium demand. In 2021, EV batteries already accounted for about 50 per cent of global lithium demand"

Similarly, cobalt demand would increase by 45 per cent to 250 kt and nickel demand would increase by 60 per cent to 4200 kt by 2030, accounting for 25 per cent and 20 per cent of the entire demand for EVs, respectively. In the aggressive scenario, the numbers increase by an additional 65%, with the proportions of EV increasing to 40% and 30%, respectively.

"To fulfil this rise in lithium demand, approximately 30 new lithium mines will be required by 2030 under the Stated Policies Scenario and 50 under the Announced Pledges Scenario, assuming an average annual lithium mine production capacity of 8 kt," the paper stated.

Moreover, this investment and expansion must occur immediately. If not, the stated objective of generating net-zero emissions in succeeding decades would not be achieved.

"By 2030, demand for lithium, nickel, and cobalt is expected to climb by 30 per cent per year, 11 per cent per year, and 9 per cent per year, respectively. In comparison, the lithium supply has expanded by 6 per cent per year over the previous five years, while the nickel supply has increased by 5 per cent per year "d cobalt by 8 per cent," it stated. "Accordingly, addressing the demand for electrification under the Net Zero Scenario necessitates substantial investments in the supply of battery materials - just as in all other clean energy technology sectors."

"As road transport electrification develops to fulfil net-zero goals, the pressure on the supply of vital materials will continue to increase. Cell components and their supply will need to expand proportionally "it added. "Additional investments are required in the near future, especially in mining, where lead times are significantly longer than in other parts of the supply chain – in some cases requiring more than a decade from initial feasibility studies to production, and then several more years to reach nominal production capacity."

"European and American governments have ambitious public sector plans to establish domestic battery supply chains, but the majority of the supply chain is likely to remain Chinese through 2030," the report stated. "China, for example, has 70 per cent of the announced battery production capacity through 2030."